Suggested citation for linking to this discussion:

U.S. Department of Agriculture, Economic Research Service. (2025, September 3). Farm sector income & finances: Assets, debt, and wealth.

Farm Sector Equity (Wealth) Forecast To Grow in 2025

Farm sector equity, the difference between farm sector total assets and total debt, is forecast to rise to $3.83 trillion in 2025, a 4.7-percent increase relative to 2024 in nominal dollars. The farm sector assets are expected to increase 4.7 percent to reach $4.42 trillion in 2025. The farm sector debt is expected to increase 5.0 percent to reach $591.8 billion in 2025. After adjusting for inflation, in 2025, farm sector equity, assets, and debt are forecast to increase by 2.1 percent, 2.1 percent, and 2.4 percent, respectively.

See the full balance sheet details, including the current/noncurrent balance sheet and selected financial ratios. A summary of the balance sheet is available in the table U.S. farm sector financial indicators, 2018–2025F.

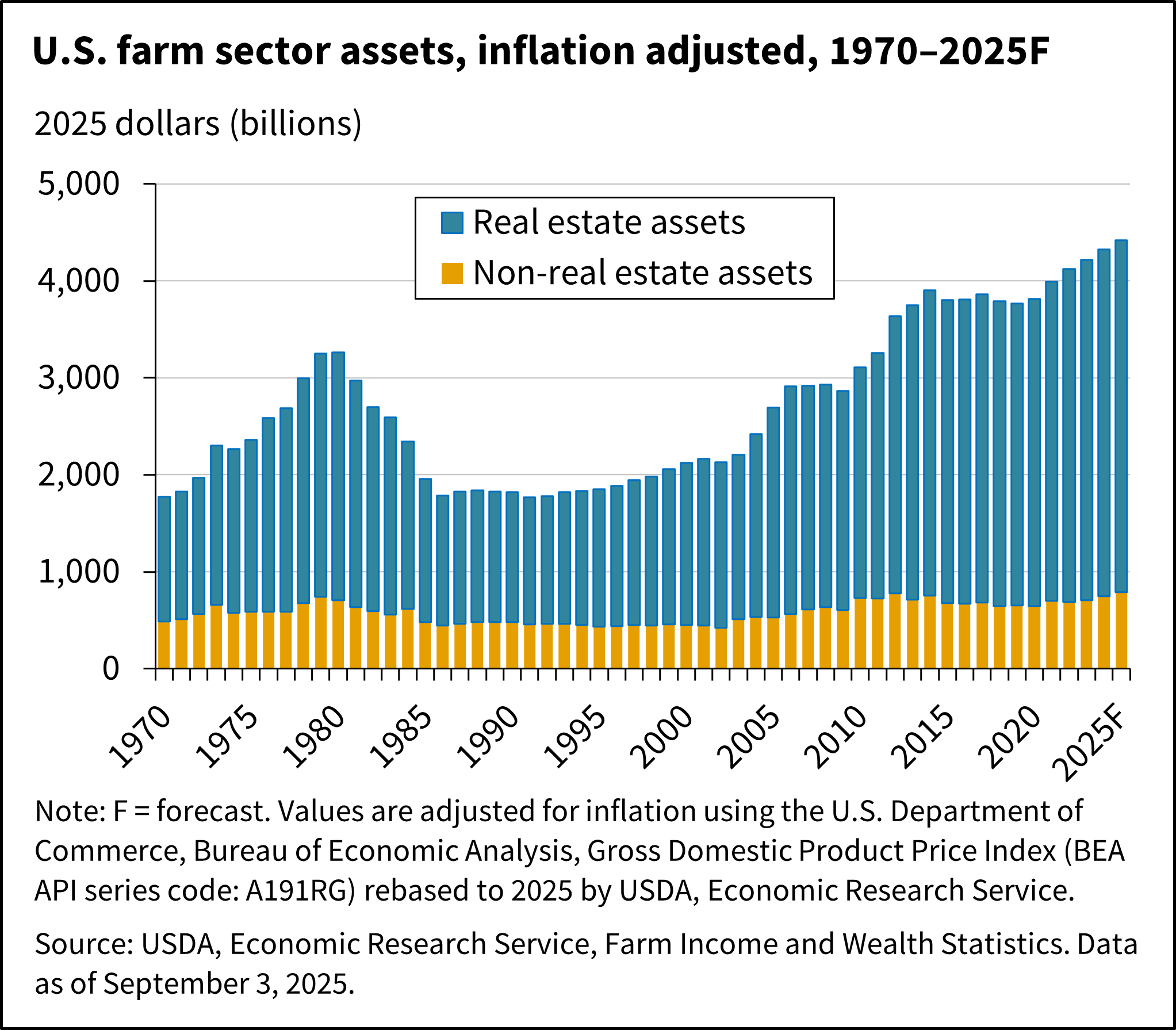

Farm real estate assets, land and its attachments, are forecast to be $3.63 trillion in 2025, a 4.0-percent increase from 2024 in nominal dollars (1.4 percent in inflation-adjusted dollars), representing 82 percent of total farm sector assets. Non-real estate assets include the value of investments and other financial assets, inventories of crops and animals, purchased inputs, and machinery/vehicles. Non-real estate assets are expected to increase 8.1 percent in 2025 in nominal dollars. In inflation-adjusted dollars, non-real estate assets are forecast to increase by 5.4 percent in 2025.

Total farm sector debt is forecast to increase in 2025 relative to 2024 with increases forecast for both real estate and non-real estate debt. Farm real estate debt is expected to reach $386.4 billion in 2025, a 5.2-percent increase in nominal dollars (2.6-percent increase in inflation-adjusted dollars) from 2024. Farm non-real estate debt is expected to reach $205.4 billion in 2025, a 4.7-percent increase in nominal terms and a 2.1-percent increase in inflation-adjusted dollars.

Farm Sector Solvency To Remain Stable and Liquidity To Improve in 2025

Farm sector solvency is forecast to remain relatively stable in 2025, with debt forecast to grow at a similar rate as assets or equity. Solvency measures the ability of a farm or ranch operation to satisfy its debt obligations when due. Popular measures of solvency include the debt-to-asset ratio and debt-to-equity ratio. Lower values for these ratios are preferred.

Liquidity is the ability to transform or convert assets to cash quickly to satisfy short-term financial obligations when due without a material loss of value or price received for the asset. The farm sector’s liquidity is forecast to improve in 2025, measured by key metrics such as working capital. Working capital measures the amount of cash available to fund operating expenses after paying off debt to creditors due within 12 months (current debt).

See selected financial ratios and more about financial ratios in the Documentation for the Farm Sector Financial Ratios.

A Note on Farm Balance Sheet Estimates and Forecasts

The farm sector balance sheet provides a market value estimate and forecast of farm sector assets, debts/other liabilities, and wealth (e.g., equity or net worth) as of December 31 of the current calendar year. It differs from individual business and corporate balance sheet accounts that are based on historical cost accounting concepts. For example, historical cost-based balance sheets show capital assets such as farm machinery and equipment at their original cost, less accumulated depreciation. The objective of the farm sector balance sheet is to estimate or forecast the value of assets if sold in today's marketplace.