Declining Crop Prices, Rising Production and Exports Highlight U.S. Agricultural Projections to 2032

- by Brian Williams, Erik Dohlman and Matthew Miller

- 2/9/2023

Highlights

- Corn, soybean, and upland cotton production and exports through 2032/33 are expected to approach or exceed record levels.

- U.S. crop prices are projected to decline in the next 3 years and then generally stabilize.

- Production and exports of beef, chicken, and pork are projected to increase over the next 10 years.

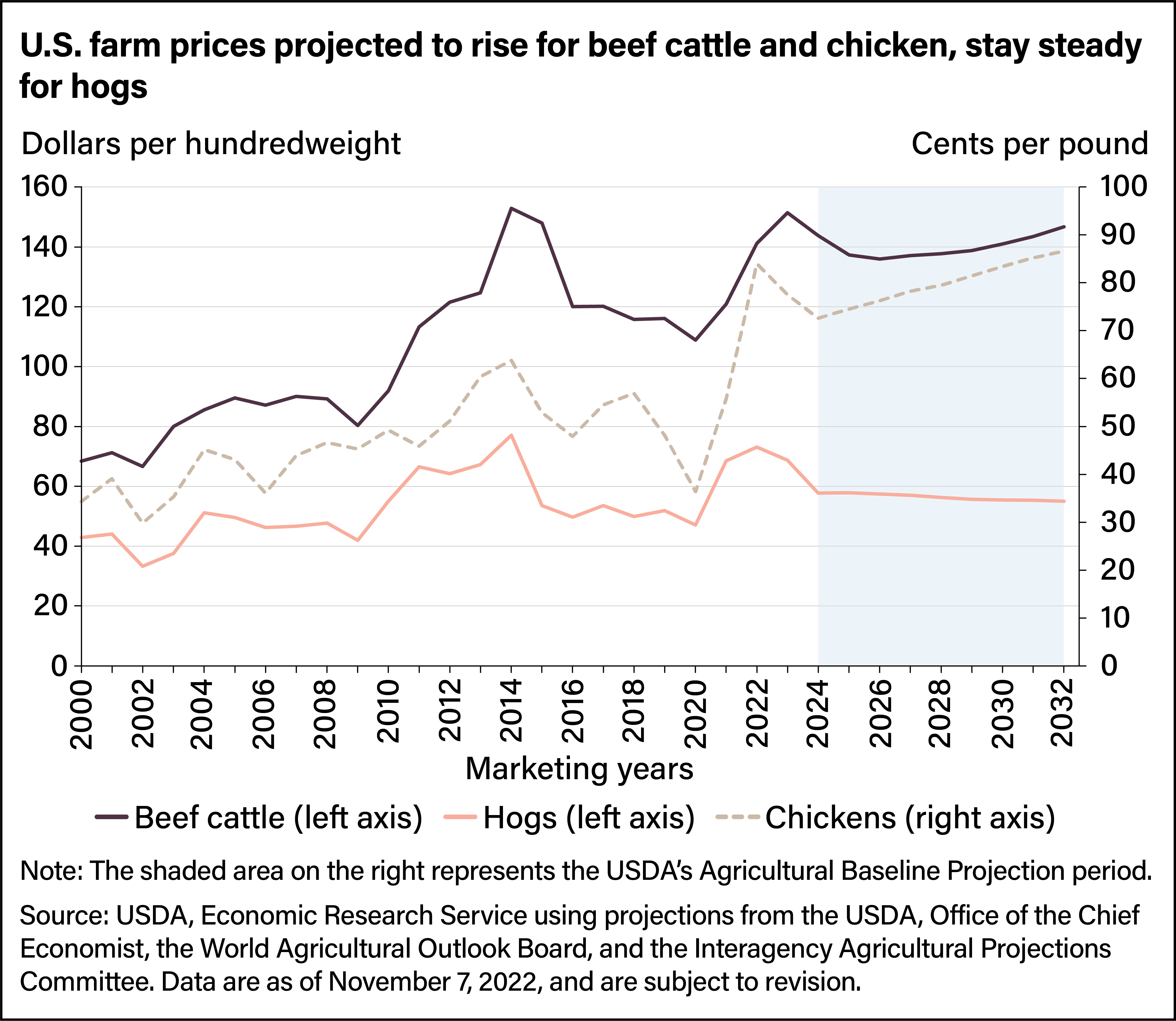

- Beef and chicken prices are projected to remain elevated, while hog prices are expected to fall.

Global economic and market conditions continue to challenge U.S. crop and livestock farming. Inflation, extreme weather events, supply chain disruptions, high input costs, and Russia's war against Ukraine have pushed commodity prices above historic trends. The situation in Ukraine has affected wheat and corn markets in particular. These conditions set the stage for the long-term outlook for U.S. and global supply, demand, and trade for major field crops (corn, soybeans, wheat, and upland cotton) and major meats (beef, pork, poultry), key commodities for gauging the performance of the U.S. farm sector.

Each year in its Agricultural Baseline Projections, USDA provides a 10-year outlook for major crop and livestock commodities based on key assumptions related to macroeconomic conditions, U.S. policy, and existing international agreements. The data include agricultural production, trade, and domestic demand projections. Projections are made assuming normal or “average” weather (without extreme weather events) and use data available as of the October 2022 World Agricultural Supply and Demand Estimates (WASDE) report and are not updated to reflect subsequent revisions (see blue box below: Making Sense of USDA Forecasts and Projections).

These projections, popularly referred to as the “Baseline,” are critical for supporting estimates of farm program spending under the President’s budget released each year by the U.S. Office of Management and Budget. In addition, the projections can be used in crop planning and investment decisions, as well as domestic and international business decisions throughout the agribusiness supply chain. For crops, the projections begin with marketing year 2023/24 and end at 2032/33. Livestock Baseline projections start with the 2024 calendar year and end in 2032. Overall, the 2023 Baseline projections offer a mixed picture for the various commodities reflecting longer term underlying trends, including income and population growth, yield growth, domestic and foreign land allocation, and dietary preferences.

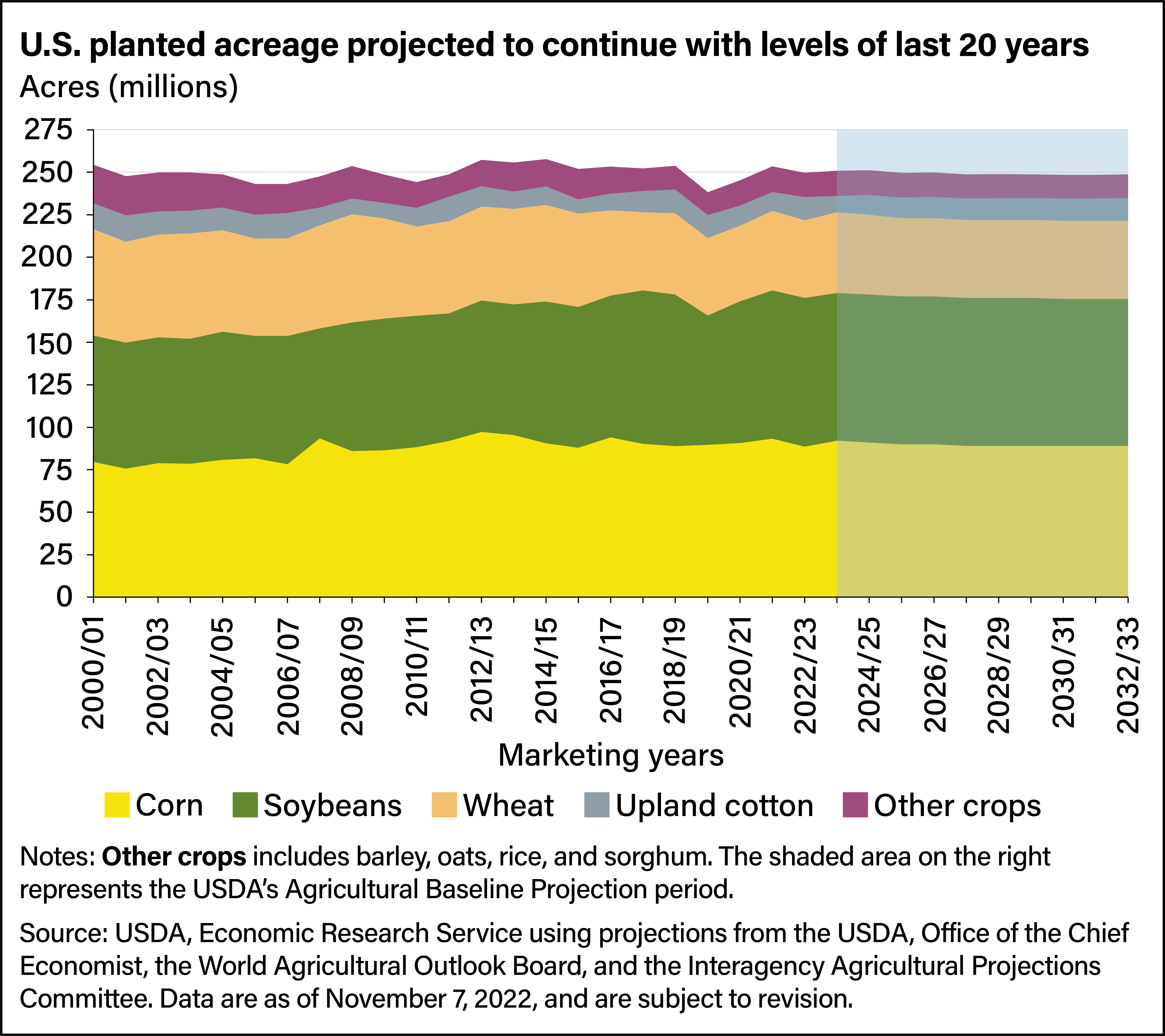

Overall U.S. Crop Area Is Expected To Remain Steady Through 2032

Despite rising prices for farm commodities, the total area planted to the eight major field crops (barley, corn, cotton, oats, rice, sorghum, soybeans, and wheat) dipped to 249.5 million acres in marketing year 2022/23 from 253.4 million acres in 2021/22 largely because of an increase in weather-related prevented plantings in 2022/23. Changes in planted acreage were led by the largest four crops—corn, soybeans, wheat, and upland cotton—which combined for more than 94 percent of the eight-crop total in 2022/23. Based on the market conditions that existed with the October WASDE, the area planted to corn is projected to rise by 3.4 million acres in 2023/24 to 92.0 million acres before tapering to 89.0 million acres by 2032/33. Soybean acreage is projected to decrease from 87.0 million in 2023/24 to 86.5 million acres by 2032/33.

Higher prices resulting from uncertainty over global wheat production and trade are projected to result in a 4-percent increase (1.8 million acres) in U.S. wheat area planted in 2023/24 to 47.5 million acres. The area planted to wheat is then projected to decline to 46.0 million acres by 2025/26 and then remain steady until 2032/33.

A decline in upland cotton prices combined with relatively favorable prices for corn—a crop often planted in rotation with cotton—is expected to result in a drop in upland cotton area planted to 9.5 million acres in 2023/24, down from 13.6 million acres planted in 2022/23 and among the lowest since 1960. The area planted to upland cotton—the dominant variety grown in the United States—is projected to recover and grow steadily after that as the global economy improves, ending with 13.3 million acres in 2032/33.

For corn, soybeans, and wheat, yields are expected to increase at rates consistent with historic trends, reflecting continuing advancements in production practices and in technology, including improvements in seed varieties and chemicals. Higher yields are expected to more than compensate for reduced planted acreage, resulting in record-high production for corn and soybeans, and increased wheat production. However, projections show wheat production remaining well below levels from most of the past two decades.

Corn yield is projected at 181.5 bushels per acre in 2023/24, up from a drought-depressed yield of 171.9 bushels in 2022/23 and is expected to continue rising to just under 200 bushels by 2032/33. Corn production is projected to grow from 15.27 billion bushels in 2023/24 to a record 16.18 billion bushels in 2032/33.

As with corn, soybean yields are expected to recover from a 4-year low of 49.8 bushels per acre in 2022/23 after dry growing conditions. Yields are expected to increase to 52.0 bushels per acre in 2023/24 and to 56.5 bushels by 2032/33. With the yield increase, soybean production is projected to grow 8 percent over the 10-year period, rising to a record 4.84 billion bushels in 2032/33.

Wheat yields are expected to return to more typical levels for 2023/24, to 49.2 bushels per acre, and to continue rising through the projection period, ending at 52.7 bushels per acre in 2032/33. However, after an initial jump in 2023/24, wheat production is projected to decline for several years, reflecting a reduction in area planted. As the number of acres planted level out, projected yield growth is expected to boost wheat production through the remainder of the projection period to just under 2.0 billion bushels. This remains less than the record of nearly 2.8 billion bushels in 1981/82.

In contrast to corn, soybeans, and wheat, upland cotton is expected to show gains in both planted area (40 percent) and yield (just more than 5 percent). With more acres planted and higher yield, cotton production is expected to grow 47 percent during the projection period, from 13.9 million bales in 2023/24 to 20.4 million bales by 2032/33.

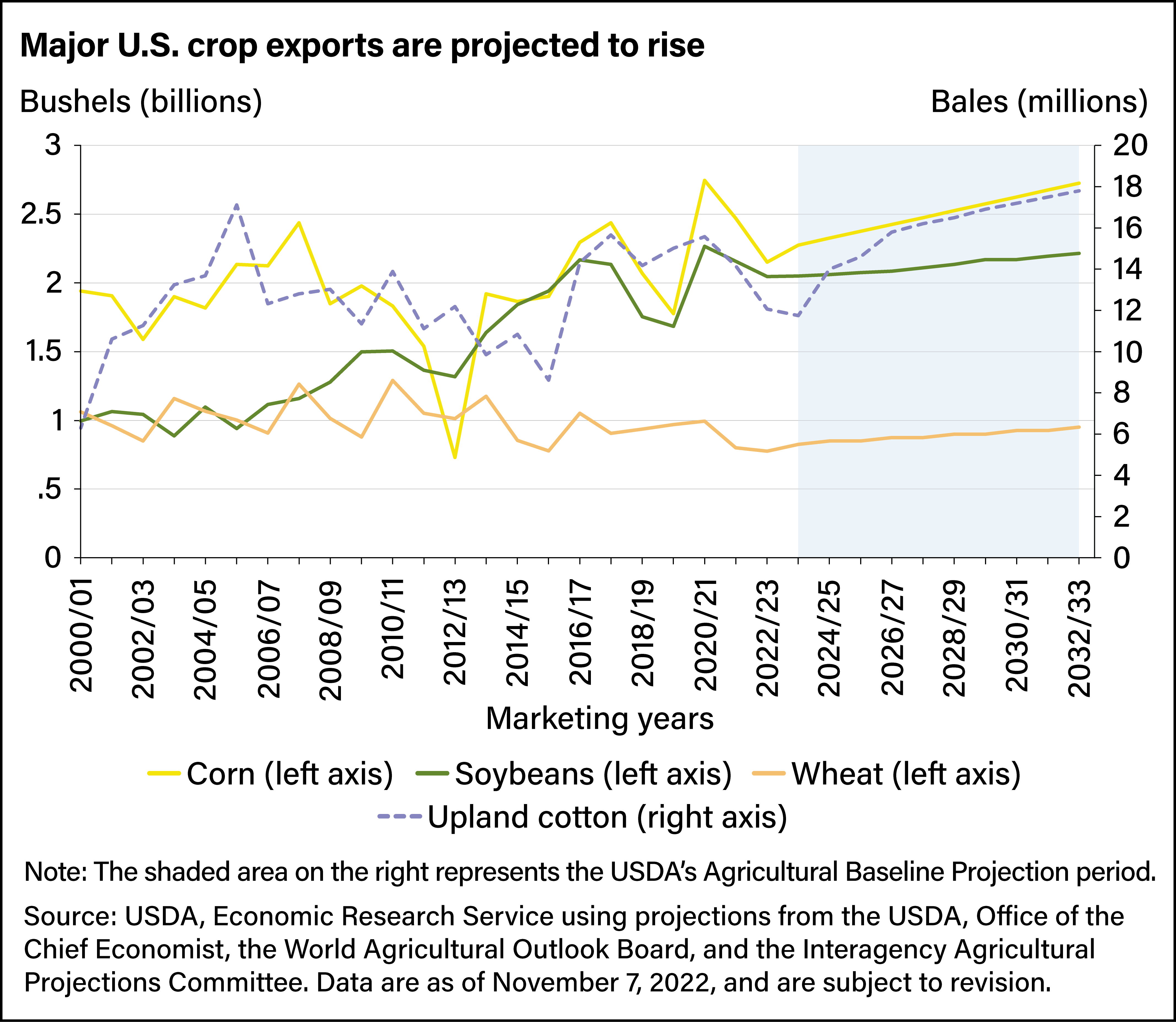

Domestic Consumption, Trade Projected To Grow for Corn, Soybeans, Wheat, and Cotton

Domestic demand for corn, soybeans, wheat, and cotton are all expected to grow over the next decade. Exports of the four crops also are expected to increase over the next decade, reaching record highs for upland cotton and near record levels for corn and soybeans. Projections show wheat exports rebounding from a projected 50-year low in 2022/23.

Domestic corn use is expected to steadily increase through the projection period, growing from 12.5 billion bushels in 2023/24 to 13.4 billion bushels by 2032/33. Driven by growth in the pork, chicken, and beef sectors (see livestock projections below), feed and residual corn use is projected to increase about 18 percent over 10 years. Use of corn for food, seed, and in industrial applications, including ethanol, is projected to decline slightly over the same period. U.S. corn exports are expected to rise nearly 20 percent from 2023/24 to 2032/33, ending at 2.7 billion bushels, which, if realized, would mark the second-highest corn export volume on record.

Soybean crush—the processing of soybeans into soybean meal and soybean oil—is expected to rise from 2.3 billion bushels in 2023/24 to 2.5 billion bushels in 2032/33. Soybean exports are expected to rise 8 percent over the projection period.

Domestic use of wheat is projected to remain relatively steady, rising 2.4 percent through 2032/33, compared with a 15-percent increase in exports over the same period. The United States also imports some wheat, mostly from Canada, to meet local demand and protein-blending requirements as a supplement to domestic supplies. Total imports are projected to range between 110 million and 120 million bushels annually.

Domestic mill use for upland cotton is expected to grow slowly over the projection period, rising nearly 9 percent from 2023/24 to 2032/33. Domestic mill use of cotton has fallen since trade barriers for imported mill products were phased out in recent decades. Use is projected at 2.5 million bales or less through 2032/33, but it exceeded 10.0 million bales during much of the 1990s. Upland cotton exports are expected to grow at a much faster rate, rising from an 8-year low of nearly 11.8 million bales in 2023/24 to 17.8 million bales in 2032/33, a 51-percent increase.

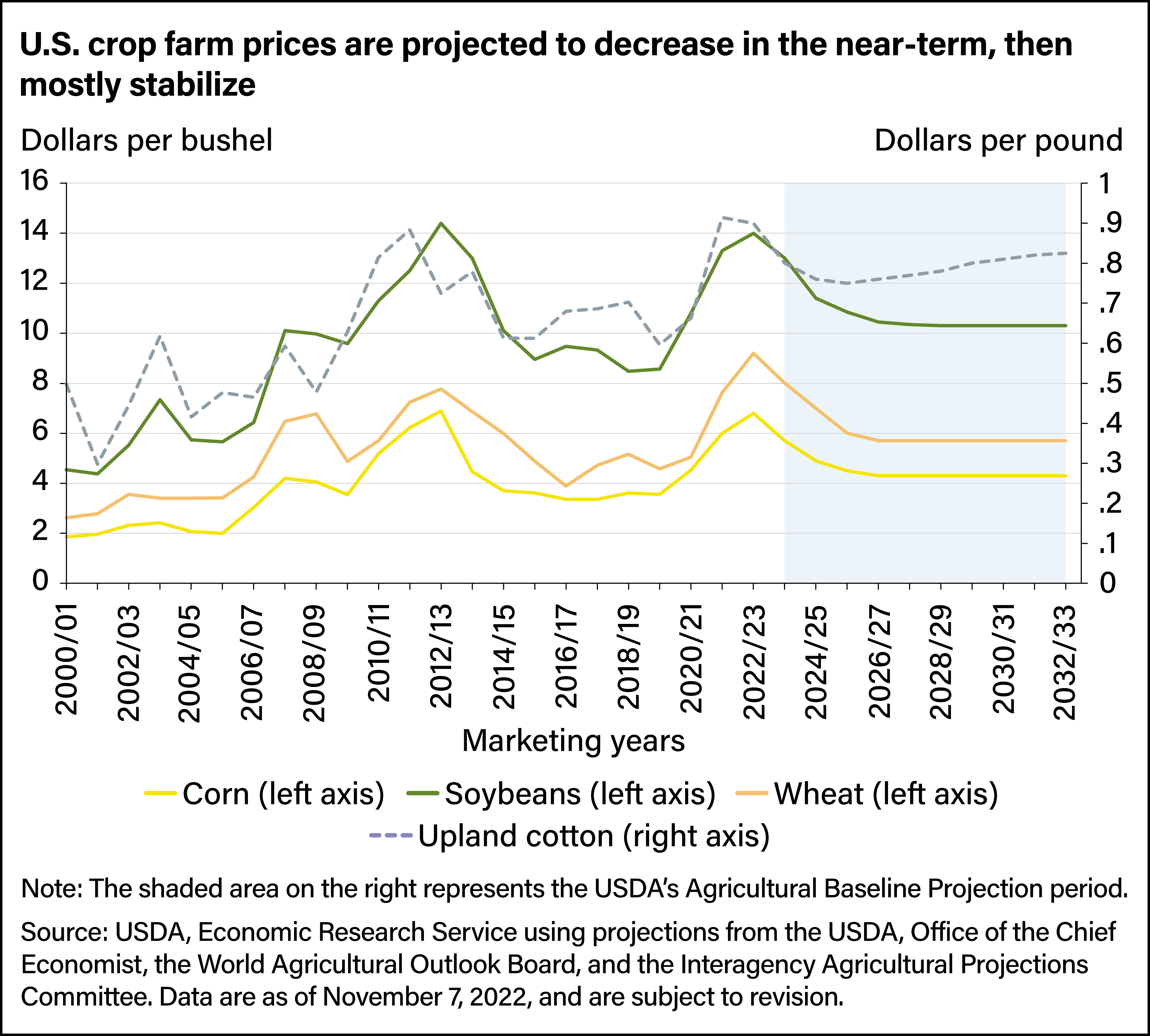

Crop Prices Generally Expected To Decline in the Near-Term, Then Stabilize

Corn prices are expected to fall from a near-record peak season average farm price of $6.80 per bushel in 2022/23 to $5.70 per bushel the following year and continue a downward trend through 2026/27 before stabilizing at $4.30. Soybean prices follow a similar trend, falling to $13.00 a bushel in the first year of the projection period, down $1.00 from the recent peak. Soybean prices are expected to continue falling through the first half of the projection period, stabilizing at $10.30 per bushel the remaining years.

Wheat prices are expected to drop from a record $9.20 a bushel in 2022/23 to $8.00 in 2023/24, still the second highest price on record. Prices are projected to continue to fall through 2026/27 before settling at $5.70 through 2032/33.

After 2 consecutive years of record or near-record highs, the price for upland cotton is expected to drop for the first year of the projection period to $0.80 per pound, down from $0.90 in 2022/23. Upland cotton prices are expected to fall further to $0.75 per pound in 2025/26 before starting a steady rise though 2032/33, ending at $0.825 per pound.

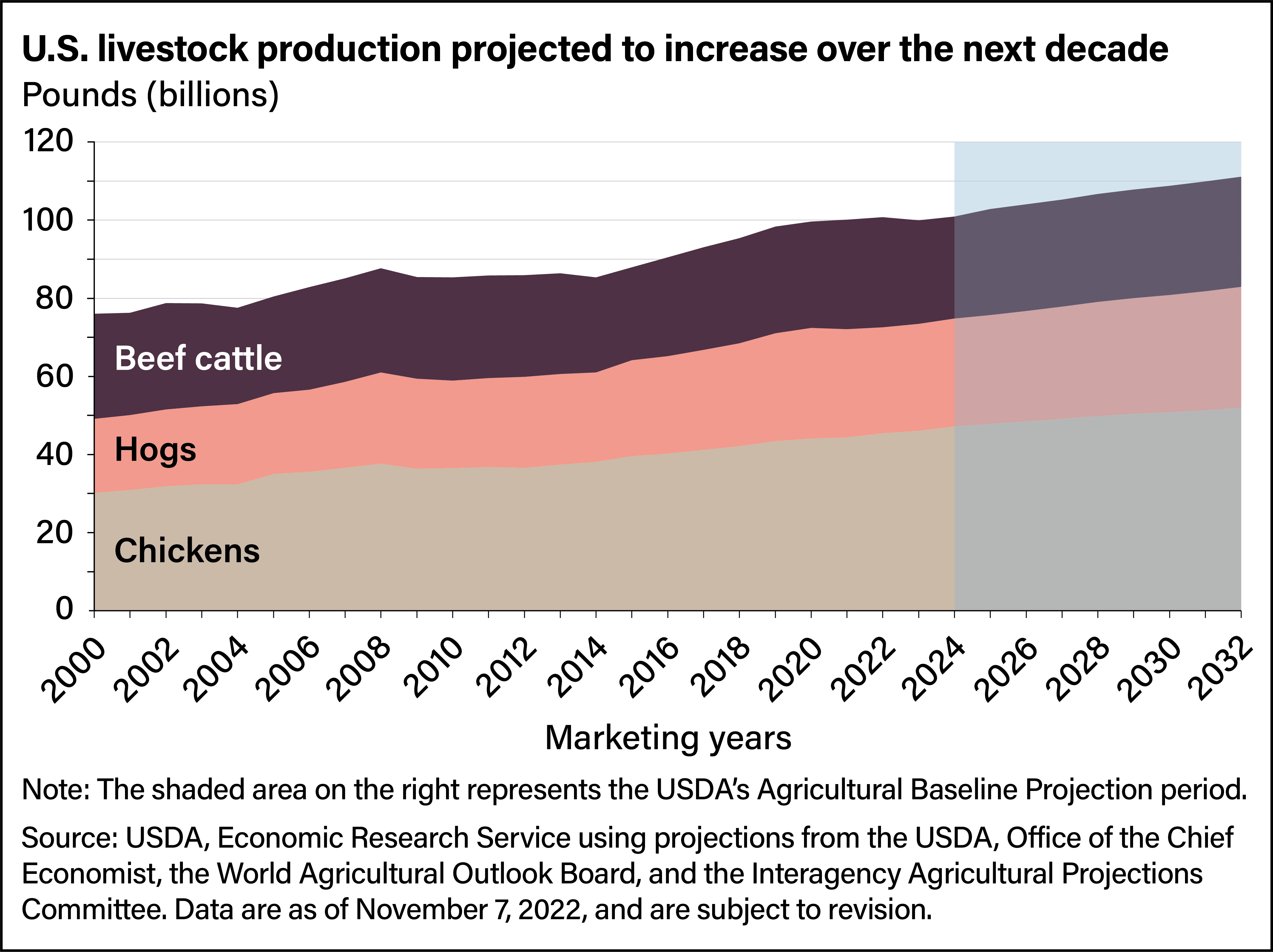

U.S. Livestock Production Expected To Continue Expanding Through 2032

Commercial beef production is projected to grow through 2032, after contracting in 2023 and 2024. Commercial slaughter volumes and weights are expected to increase, expanding production to record levels by 2032. Beginning at 26.0 billion pounds in 2024, production is projected to grow to 28.1 billion pounds in 2032.

Commercial pork production is also projected to increase over the 10-year projection period, driven by rising hog inventories as producers increase supply to meet processor demand. Total commercial production of pork is projected to grow from 27.6 billion pounds in 2024 to a record 30.9 billion pounds in 2032, a 12-percent increase.

Chicken production is expected to follow a similar pattern, growing 10 percent over the projection period to a record 52.0 billion pounds in 2032.

Beef, Pork, Chicken Exports Each Expected To Climb to Record or Near-Record Levels by 2032

Of the three meats, exports for chicken—one of the cheapest sources of animal protein globally—are expected to be notably strong. Chicken exports are expected to rise almost 13 percent from 7.5 billion pounds in 2024 to a record 8.4 billion by 2032. As the U.S. cattle herd is rebuilt after a higher-than-normal rate of slaughter in 2022 during drought conditions, beef exports are expected to decline in 2023 and 2024 and then rise during the remainder of the projection period, reaching near-record levels in 2032 at 3.3 billion pounds. Pork exports are projected to climb throughout the period, approaching record levels as they rise from 6.3 billion pounds in 2024 to 6.9 billion in 2032.

The United States is a significant importer of beef, with import volumes often similar to those of its exports. The country sends a surplus of higher value cuts of feedlot-finished beef to Europe and Asia and imports lower value lean beef to supplement the domestic production of ground beef. To support domestic consumption, U.S. beef imports are expected to rise to 3.6 billion pounds in 2024 but decline after, hovering around 3.1 billion to 3.2 billion pounds annually. If realized, beef imports would still be above the annual average of the prior two decades.

The United States is also a significant importer of pork, although exports still outweigh imports. Pork imports increased rapidly in recent years, rising from a recent low of 904 million pounds in 2020 to a projected 1.477 billion in 2022. Imports are expected to grow to a record 1.683 billion pounds by 2032, boosted by a strong U.S. dollar and an influx of Canadian pork that had historically been exported to China.

In the near term, farm prices (not adjusted for inflation) for all animals and animal products are projected to fall from recent record or near-record levels set in 2022. After an initial decline, cattle prices are expected to rise steadily after 2026. Hog prices are expected to decline through most of the projection period, with the farm price for hogs in 2032 almost 5 percent lower than in 2024. By the end of the projection period, chicken prices are expected to approach record levels, with farm prices for broilers (young chickens) rising 19 percent.

This article is drawn from:

- Agricultural Baseline Database. (n.d.). U.S. Department of Agriculture, Economic Research Service.