Local Food Sales Continue to Grow Through a Variety of Marketing Channels

Local foods represent a small but growing share of the U.S. food system—one reflection of consumers’ increasing influence on food production. Local food producers sell their goods directly to consumers at places such as farmers markets, on-farm stores, or pick-your-own stores. They also sell to retailers such as restaurants or grocery stores, institutions such as schools, universities, or hospitals, and intermediaries such as processors or wholesalers. Local and regional food systems provide significant income for many farmers, which supports rural communities, beginning farmers, and small-scale farmers. According to data from the USDA, National Agricultural Statistics Service (NASS), sales of local edible farm products in 2017 totaled $11.8 billion, or 3 percent of all agricultural sales in 2017, up from $8.7 billion in 2015.

Historically, local farmers have mostly sold their products directly to consumers in farmers markets or other dedicated outlets. As directed under the 2014 Farm Bill, NASS conducted a first-time survey to produce official benchmark data on the local food sectors in all 50 States. Researchers from the USDA, Economic Research Service (ERS) recently used data from this survey, conducted in 2016, to evaluate how local food farmers of varying levels of experience responded to an increasing demand for local food as documented in earlier studies.

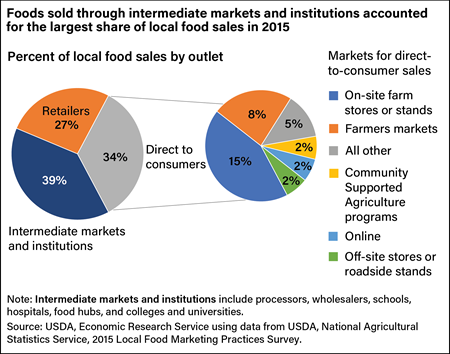

An ERS report and other studies show that a higher percentage of local food sales in 2015 were through retailers, institutions, and intermediate markets, rather than directly to consumers. The survey showed most local foods were sold through intermediate markets and institutions (39 percent), followed by direct-to-consumer (34 percent) and retailers (27 percent). Researchers have found that most of the growth in local food sales has come through intermediaries, institutions, and retailers as the growing popularity of these markets has led to a plateau in direct-to-consumer sales. For example, a 2018 article in the journal Ecological Economics indicates that consumers are not willing to pay a premium for local food at farmers markets compared to grocery stores. According to the article, this is possibly because of limited product offerings at farmers markets and increases in the time and effort to fulfill grocery needs since consumers may need to shop at multiple locations.

Observers often gauge the popularity of local foods by growth in the number of farmers markets. However, on-site farm stores and farm stands were by far the most popular marketing channel for direct-to-consumer sales in 2015. On-site farm stores or stands accounted for 15 percent of all local food sales that year, and 31 percent of farms with local food sales had on-site farm stores or stands. Eight percent of all local food sales were through farmers markets, and 25 percent of farms selling local food used this marketing channel in 2015. Twenty-four percent of farms with local food sales in 2015 sold through other types of direct-to-consumer outlets—such as pick-your-own or mobile markets—and those sales made up 5 percent of total local food sales.

Only 6.4 percent of local food producers sold through all four direct marketing channels (consumers, retailers, institutions, and intermediate markets). Farmers with different levels of farming experience may prefer certain direct marketing channels over others. For example, farmers with 10 or fewer years of farming experience may find it easier to enter the direct-to-consumer marketing channel than other marketing channels. Increased understanding of how farmers sell local foods can inform future programs and policies to support local foods and beginning farmers.

Marketing Practices and Financial Performance of Local Food Producers: A Comparison of Beginning and Experienced Farmers, by Stephen Martinez and Timothy Park, ERS, August 2021

Trends in U.S. Local and Regional Food Systems: A Report to Congress, by Sarah A. Low, Aaron Adalja, Elizabeth Beaulieu, Nigel Key, Stephen Martinez, Alex Melton, Agnes Perez, Katherine Ralston, Hayden Stewart, Shellye Suttles, Stephen Vogel, and Becca B.R. Jablonski, USDA, Economic Research Service, January 2015

Local Food Systems: Concepts, Impacts, and Issues, by Stephen Martinez, Michael S. Hand, Michelle Da Pra, Susan Pollack, Katherine Ralston, Travis Smith, Stephen Vogel, Shellye Clark, Luanne Lohr, Sarah A. Low, and Constance Newman, USDA, Economic Research Service, May 2010

ARMS Farm Financial and Crop Production Practices, by ARMS Team, USDA, Economic Research Service, December 2023